Filing your Income Tax Return (ITR) is an essential part of financial planning and tax compliance. However, many taxpayers are confused about which ITR form they should use. Choosing the correct ITR form helps ensure accurate tax filing, faster processing, and reduces the chances of receiving notices from the Income Tax Department.

In this guide, we’ll explain each ITR form, who can file it, and how to determine the right one for your income sources.

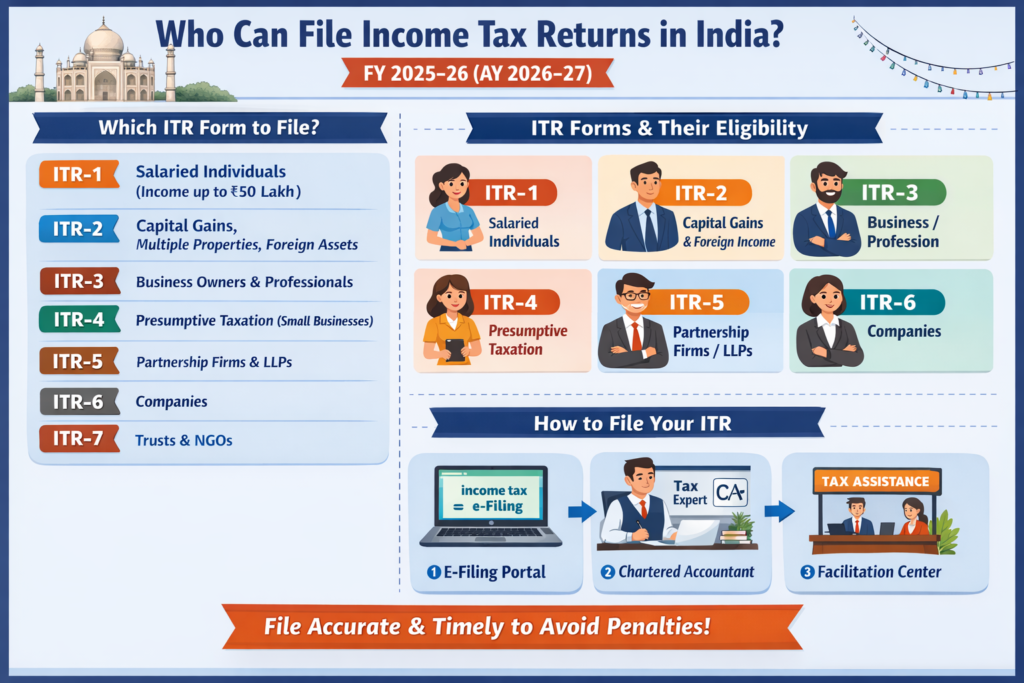

Quick Summary: Which ITR Form Should You File?

| ITR Form | Suitable For |

| ITR-1 (Sahaj) | Salaried individuals with income up to ₹50 lakh and simple income sources |

| ITR-2 | Individuals with capital gains, foreign assets, or multiple properties |

| ITR-3 | Business owners, professionals, freelancers, and traders |

| ITR-4 (Sugam) | Taxpayers opting for presumptive taxation |

| ITR-5 | Firms, LLPs, AOPs, and BOIs |

| ITR-6 | Companies |

| ITR-7 | Trusts, NGOs, and charitable institutions |

What Is an Income Tax Return (ITR)?

An Income Tax Return (ITR) is a form used by taxpayers to report their income, deductions, investments, and taxes paid during a financial year to the Income Tax Department of India.

The Income Tax Department has prescribed different ITR forms based on the taxpayer’s income source, residential status, and category.

Types of Income Tax Return (ITR) Forms in India and who can file these.

1. ITR-1 (Sahaj)

Who Can File ITR-1?

ITR-1 is designed for resident individuals whose total income does not exceed ₹50 lakh and includes:

- Salary or pension income

- Income from one house property

- Income from other sources (such as savings account interest or fixed deposit interest)

- Agricultural income up to ₹5,000

Who Cannot File ITR-1?

You cannot use ITR-1 if:

- Your total income exceeds ₹50 lakh

- You have capital gains from shares, mutual funds, property, or other assets

- You own more than one house property

- You have foreign income or foreign assets

You earn income from a business or profession

2. ITR-2

Who Can File ITR-2?

ITR-2 is suitable for individuals and Hindu Undivided Families (HUFs) who do not have income from business or profession.

Suitable For:

- Salaried individuals having an income of more than Rs. 50Lac

- Individuals with multiple house properties

- Taxpayers earning capital gains from: ( Not in case of purchase, but in case of Sales)

- Stocks

- Mutual Funds

- Real Estate

- Gold

- Individuals with foreign assets or foreign income

- Agricultural income exceeding ₹5,000

3. ITR-3

Who Can File ITR-3?

ITR-3 is meant for individuals and HUFs earning income from a business or profession.

Suitable For:

- Proprietors

- Freelancers

- Consultants

- Doctors

- Lawyers

- Chartered Accountants

- Traders engaged in intraday trading or Futures & Options (F&O) trading

Bookkeeping Requirement

Taxpayers filing ITR-3 are generally required to maintain proper books of accounts and supporting documents as prescribed under the Income Tax Act. These records help in accurately reporting income, expenses, profits, and tax liabilities. Depending on the nature and turnover of the business or profession, taxpayers may also be subject to a tax audit under applicable provisions.

4. ITR-4 (Sugam)

Who Can File ITR-4?

ITR-4 is designed for resident individuals, HUFs, and firms (excluding LLPs) who opt for the presumptive taxation scheme.

Applicable Under:

- Section 44AD – Presumptive taxation for businesses

- Section 44ADA – Presumptive taxation for professionals

- Section 44AE – Presumptive taxation for transport businesses

Conditions:

- Eligible under the presumptive taxation scheme

- Income within the prescribed limits under the applicable provisions

- Simplified tax return filing process

5. ITR-5

Who Can File ITR-5?

ITR-5 is applicable to:

- Partnership Firms

- Limited Liability Partnerships (LLPs)

- Association of Persons (AOPs)

- Body of Individuals (BOIs)

Example:

A partnership firm engaged in trading activities should file ITR-5.

6. ITR-6

Who Can File ITR-6?

ITR-6 is meant for companies that are not claiming exemption under Section 11 of the Income Tax Act.

Section 11 of the Income Tax Act, 1961 – Exemption for Charitable and Religious Trusts

Section 11 of the Income Tax Act provides tax exemption on income derived from property held under a trust or institution established for charitable or religious purposes.

Who Can Claim Exemption Under Section 11?

The exemption is available to:

- Charitable trusts

- Religious trusts

- Registered non-governmental organizations (NGOs)

- Educational institutions

- Hospitals and medical institutions

- Other institutions registered under the relevant provisions of the Income Tax Act

Example:

A private limited company engaged in business operations should file ITR-6.

7. ITR-7

Who Can File ITR-7?

ITR-7 is applicable to entities required to file returns under specific sections of the Income Tax Act, including:

- Charitable Trusts

- Religious Institutions

- Educational Institutions

- Political Parties

- Research Associations

Example:

A charitable trust registered under the Income Tax Act should file ITR-7.

Important Note for Stock Market Investors

Many investors file the wrong ITR form, which can lead to compliance issues. Here’s a quick guide:

- Capital gains from stocks, mutual funds, ETFs, or property → ITR-2

- Intraday stock trading income → ITR-3

- Futures and Options (F&O) trading income → ITR-3

- Eligible trading income under presumptive taxation → ITR-4

Understanding this distinction is crucial because capital gains and trading income are treated differently under Indian tax laws.