The popularity of mutual funds is growing rapidly, especially among beginners who do not want to directly pick stocks or bonds and may not have enough time to study company financials in detail. If you are new to investing and want to build at least a basic understanding of the product you may soon invest in, you are in the right place.

At first, terms like SIP, NAV, equity funds, debt funds, and expense ratio may sound confusing. But once you understand them in a simple way, mutual funds can become a smooth and effective way to start your investment journey.

As a beginner, there are a few important things you should know, such as:

- What is a mutual fund?

- How does it work?

- What are its types?

- What are its benefits?

- What are its risks?

- And finally, how can you start investing in mutual funds in India?

What Is a Mutual Fund?

A mutual fund is an investment vehicle that pools money from many investors. This money is then invested by a fund manager in a diversified portfolio of assets such as stocks, bonds, government securities, money market instruments, gold-related instruments, or a mix of these, depending on the objective of the scheme.

In simple words, instead of buying shares or bonds on your own, you invest your money in a mutual fund scheme. That money is then managed by a professional expert called a fund manager. On your behalf, the fund manager invests the money according to the scheme’s objective, with the aim of generating returns while managing risk.

Simple Example

Imagine there are three baskets, and you decide to invest in the third basket. The money of all investors who want to invest in that basket is collected together. A professional fund manager then manages that basket.

In return, you receive units based on the amount you invest. These units are similar to shares, except that in mutual funds you own units of the scheme. Any profit or loss from the basket is shared among investors according to the number of units they hold.

One of the best things about mutual funds is that you can start with even a small amount and still get access to a professionally managed and diversified portfolio, without becoming a market expert yourself.

How Does a Mutual Fund Work?

Let’s understand how a mutual fund works step by step.

1. Investors Put Money Into a Mutual Fund Scheme

When you invest in a mutual fund, your money is pooled together with the money of many other investors.

2. The Fund Issues Units to Investors

The mutual fund uses the NAV (Net Asset Value) on the day of investment to allot units to investors.

NAV Formula

NAV = (Total value of assets – liabilities and expenses) ÷ total number of units outstanding

Example

Suppose:

- You invest ₹5,000

- The mutual fund’s NAV is ₹20

Then the number of units allotted to you will be:

₹5,000 ÷ ₹20 = 250 units

So, your holding in that mutual fund will be 250 units.

3. The Fund Manager Invests the Pooled Money

The fund manager invests the pooled money according to the objective of the scheme.

For example:

- Equity fund → invests in shares of listed companies

- Debt fund → invests in bonds, treasury bills, and fixed-income instruments

- Hybrid fund → invests in both equity and debt

4. The Value of Investments Changes Daily

The value of the underlying investments changes every day based on market conditions. This directly affects the fund’s NAV, which also changes accordingly.

5. You Earn Returns if the Fund Value Grows

If the value of the fund’s investments rises, your investment value increases. If the value falls, your investment value also declines.

And remember: do not judge a mutual fund scheme only by its NAV. A lower NAV does not mean the fund is cheaper or better, and a higher NAV does not mean it is expensive.

Think of it this way: sometimes you pay more for a quality product, and sometimes you get a quality product at a lower price. NAV alone does not tell the full story.

Why Do Most People Invest in Mutual Funds?

Mutual funds are popular for many reasons, especially among beginners. Here are some of the biggest benefits:

1. Professional Management

Mutual funds are managed by qualified and experienced professionals.

2. Diversification

A mutual fund spreads your money across different investments, which helps reduce the impact of poor performance from a single stock or bond.

3. You Can Start With a Small Amount

Many mutual funds allow you to start with as little as ₹500.

4. Convenience

Mutual funds are easy to invest in and manage. You can:

- invest online

- track your portfolio

- redeem units

- automate investments through SIPs

5. Goal-Based Investing

Mutual funds can help you invest for different financial goals, such as:

- wealth creation

- tax saving

- short-term parking of money

- retirement planning

- child education planning

- regular investing through SIPs

6. Potential to Beat Inflation

Certain mutual funds, especially equity-oriented ones, may offer returns that can beat inflation over the long term.

Return over the period can be calculated through the SIP Calculator

Types of Mutual Funds in India

1. Equity Mutual Funds

Equity mutual funds are suitable for long-term goals and for investors who can handle market ups and downs.

Examples:

- Large Cap Funds

- Mid Cap Funds

- Small Cap Funds

- Flexi Cap Funds

- Index Funds

- ELSS Funds

2. Debt Mutual Funds

Debt funds invest in fixed-income instruments such as:

- government securities

- corporate bonds

- treasury bills

- money market instruments

They are generally less volatile than equity funds, but they are not risk-free.

3. Hybrid Mutual Funds

Hybrid funds invest in a mix of equity and debt. They can be useful for beginners who want a balance between growth and stability.

4. Index Funds

Index funds aim to track a market index such as the Nifty 50 or Sensex.

5. ELSS Funds

ELSS (Equity Linked Savings Scheme) is a tax-saving mutual fund that qualifies for deduction under Section 80C under the old tax regime, subject to applicable tax rules. It comes with a 3-year lock-in period.

Risks of Mutual Funds

Mutual funds are definitely useful, but like all investments, they are not risk-free. The main risks include:

1. Market Risk

Equity mutual funds can fall in value when stock markets decline.

2. Interest Rate and Credit Risk

Debt funds may be affected by interest rate changes or issues related to bond issuers.

3. Wrong Fund Selection

Even a good fund may be unsuitable if it does not match your time horizon, financial goal, or risk appetite.

Example:

Taking a sports bike to buy groceries in heavy rain may sound exciting, but it is probably not the smartest choice. In the same way, a good mutual fund can still be the wrong choice if it does not suit your needs.

What Is SIP in Mutual Funds?

The word SIP has become very popular among investors. Whether you choose SIP or lump sum, both are simply ways of investing money into a mutual fund.

SIP (Systematic Investment Plan)

A SIP is a way of investing a fixed amount in a mutual fund at regular intervals, usually every month.

For example:

- ₹500 per month

- ₹1,000 per month

- ₹5,000 per month

Lump Sum

A lump sum investment means investing a larger amount at one time.

It may be suitable if you already have surplus money available for investing.

Both methods can work well. The better choice depends on your cash flow, financial goal, and comfort level.

How to Start Investing in Mutual Funds in India

Starting a mutual fund investment is now quite simple and can be done through a demat account as well.

Step 1: Complete Your KYC

You usually need:

- PAN

- Aadhaar or another valid ID proof

- address proof

- bank details

Step 2: Choose SIP or Lump Sum

Decide whether you want to invest regularly or in one go.

Step 3: Select a Suitable Fund

Pick a mutual fund based on your:

- financial goal

- risk appetite

- time horizon

Step 4: Invest Through a Platform

You can invest through:

- AMC websites/apps

- registered investment platforms

- banks or authorized distributors

Common Mutual Fund Terms Beginners Should Know

NAV

Net Asset Value, or the per-unit value of a mutual fund.

SIP

Systematic Investment Plan, a way to invest regularly.

Expense Ratio

The annual fee charged by the fund for managing your money.

Exit Load

A fee charged if you redeem units within a specified period.

AUM

Assets Under Management, which shows the total value of money managed by the fund.

These can be easily checked on Moneycontrol.

Common Mistakes Beginners Should Avoid

- Investing without a clear goal is like boarding a train without checking where it is going.

- Choosing funds only based on recent returns is like choosing a cricket captain because he hit one lucky six in the previous match.

- Ignoring risk level is like ordering the spiciest dish on the menu without asking how spicy it actually is.

- Stopping SIPs in panic during market falls is like cancelling your gym membership after one week because you did not get abs immediately.

- Investing short-term money in high-risk equity funds is like taking your wedding outfit to a Holi party and hoping it stays clean.

- Buying too many similar funds without understanding overlap is like ordering paneer butter masala from six different restaurants and calling it a balanced diet.

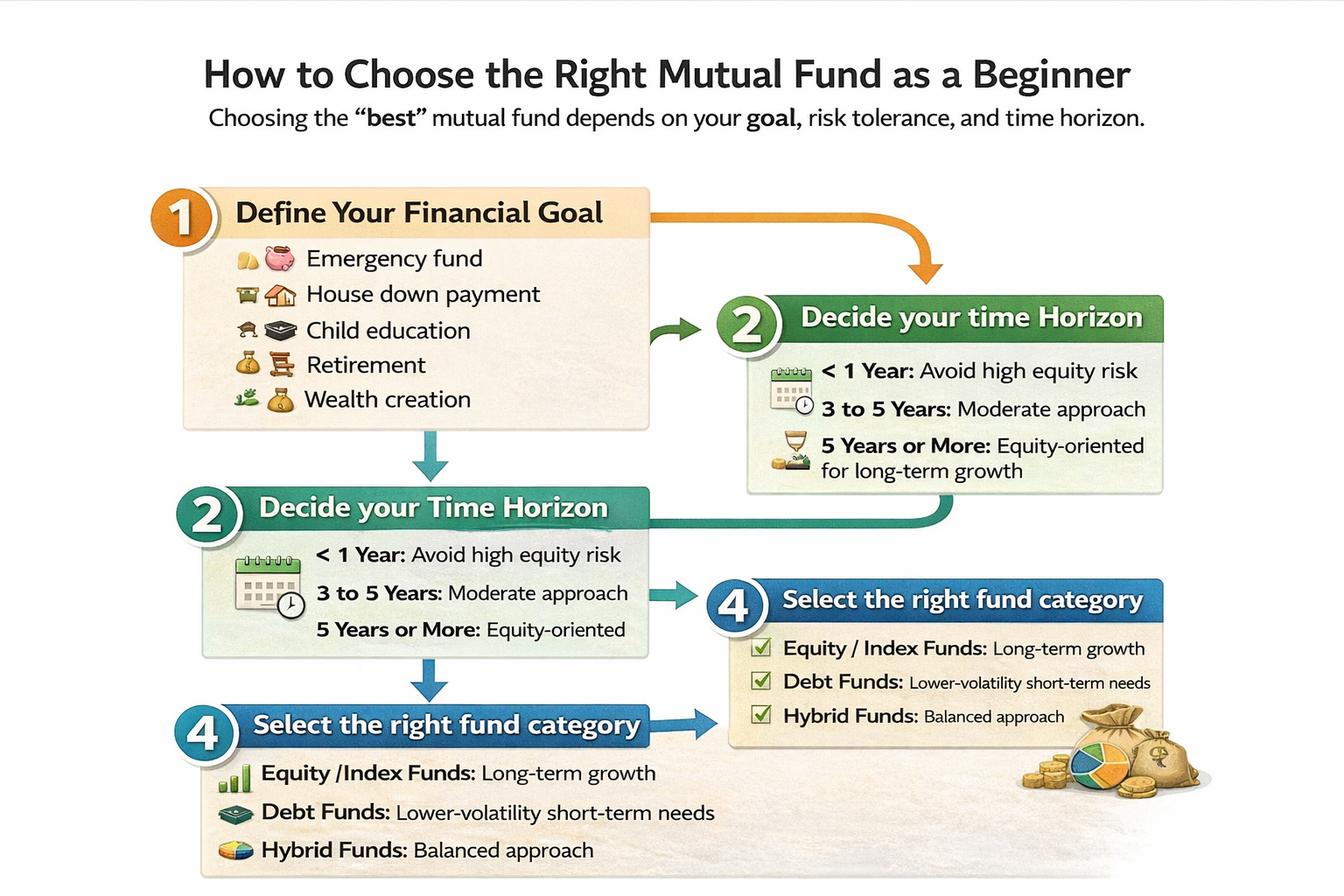

How to Choose the Right Mutual Fund as a Beginner

The meaning of choosing the “best” mutual fund is it should depend on your goal, risk tolerance, and time horizon, and its not about picking the fund with the highest recent return.

Step 1: Define your financial goal

Ask yourself why you are investing, reasons can be anything like

- emergency fund

- child education

- retirement

- wealth creation

- Payment for new house

Step 2: Decide your time horizon

- less than 1 year → avoid taking high equity risk for near-term needs

- 3 to 5 years → moderate approach depending on goal

- 5 years or more → equity-oriented funds may be considered for long-term growth, subject to suitability

Step 3: Understand your risk appetite

Can you handle temporary declines in portfolio value without panicking? If not, then go for conservative allocation.

Step 4: Choose the right category first

For example:

- long-term growth → equity or index funds, depending on suitability

- lower-volatility short-term needs → certain debt categories, depending on the time horizon and risk

balanced approach → hybrid funds

Step 5: Compare the fund carefully

Check:

- investment objective

- fund category

- benchmark

- expense ratio

- portfolio quality

- fund manager track record

- consistency across market cycles

- riskometer / risk level

- exit load

- suitability for your goal